The NIH OHR office has compiled a list of FAQs surrounding retirement. These FAQs have been divided by benefits topic. You are strongly encouraged you to read through this information if you have questions about your benefits in retirement.

For Information on Discontinued Service Retirements, please go to our Fact Sheet.

Voluntary Early Retirement Authority (VERA)

Please note that employees who are eligible for an unreduced optional retirement do not benefit from a VERA.

For VERA specific information, review our Fact Sheet.

- Does VERA eligibility change the eligibility for regular optional retirement? No.

- If I take the VERA, will my annuity be reduced? CSRS employees will have a reduction in their annuity of 2% per year for each year under age 55. The reduction is permanent. FERS employees will not have a reduction under a VERA.

- If I take the VERA, will I be eligible for the FERS Annuity Supplement? Yes, when you reach your MRA.

- I know the FERS Supplement is subject to the Social Security earnings test. Is there a calculator? Yes, use the Retirement Earnings Test calculator. You may also visit this webpage to learn more about how the earnings test works: Exempt Amounts Under the Earnings Test

- How do I know if I have enough time in service to meet the requirements to retire? You can check your information in GRB, but it's recommended to contact the Benefits Office at AskBenefits@nih.gov before making a decision to accept a VERA.

- If I accept the VERA only, what is the effective date of my retirement? You can choose a retirement date between March 17, 2025, and April 19, 2025.

- What if I am not eligible for VERA until after April 19, 2025? If you become eligible for VERA between April 19, 2025, and May 9, 2025, you must retire on the date you become eligible.

- What if I am not eligible for VERA until after April 19, 2025? If you become eligible for VERA between April 19, 2025, and May 9, 2025, you must retire on the date you become eligible.

- If I accept the VSIP and retire under VERA, what is the effective date of my retirement? If you are eligible for VERA by April 19, 2024, you must retire by this date. If you first become eligible for VERA between April 20, 2025, and May 9, 2025, you must retire on the date you meet eligibility. If you become eligible after 05/09/2025, you are not eligible for VERA.

- Can I delay the date of my retirement? No.

- I took the VERA and not the VSIP. Am I entitled to 8 weeks of administrative leave? No. The 8 weeks of administrative leave is connected only to the VSIP.

- How do I apply for the VERA? You are able to express your interest in the VERA program by completing the HHS VERA Intake Form. This is the form that is required to meet the HHS VERA program deadline by Friday, March 14, 2025.

- Where can I obtain retirement paperwork if my VERA is accepted? Visit the NIH retirement page for FERS or CSRS application instructions. Your retirement application must be submitted to the NIH Benefits Office by 03/31/2025, but only the HHS VERA Intake Form is required by 03/14/2025.

- Where can I learn more about VERA? Visit OPM's Voluntary Early Retirement Authority webpage or our Fact Sheet.

- I'm eligible for unreduced regular retirement. Am I eligible for VERA? No.

- I'm eligible for MRA+10 but I don't meet eligibility for VERA. What are my options? You can continue working or retire under MRA+10 provisions. You may also postpone your MRA+10 retirement to reduce or eliminate the age reduction. If you do this, your separation is processed as a resignation. You will need to submit the RI 92-19 to OPM three months prior to the date you want to draw your annuity.

- I am Title 42. Can I take the VERA?

- Title 42(g) - appointment has a specific time limit, therefore is not eligible for VSIP and/or VERA

- Title 42(f) - if appointment has a specific time limit, then not eligible for VSIP and/or VERA

- Title 42(f) - if appointment does not have a specific time limit (indefinite), the eligible for VSIP and/or VERA, provided other requirements are met for these incentives such as, being employed by the Executive Branch of the Federal Government for a continuous period of at least 3 years.

- How do I obtain my retirement papers to submit to the Benefits Office? Refer to the OHR Retirement page to locate the checklist for the retirement paperwork.

- I need help accessing GRB. Contact the GRB Helpdesk at Government Retirement and Benefits (GRB) Platform | Office of Human Resources.

Additional FAQs can be found in our OHR FAQ Sheet.

Voluntary Separation Incentive Payment (VSIP)

- Where can I learn general information about VSIPs? You can go to OPM's website.

- What is the deadline to show interest in the VSIP? Friday, March 14, 2025, at 5 PM EST.

- How do I apply for the VSIP? You will submit the HHS VSIP Intake Form. You will not get a confirmation email, but you should get a message letting you know the form was received after submission.

- I am interested in the VERA being offered. Can I apply for the VSIP too? Yes. You will need to submit the VSIP Interest Form.

- I am eligible for regular retirement and wish to apply for the VSIP. I have not had FEHB for 5 years prior to the retirement date. Has OPM granted a waiver for this? Yes.

- I am Title 42. Can I take the VSIP?

- Title 42(g) - appointment has a specific time limit, therefore is not eligible for VSIP and/or VERA

- Title 42(f) - if appointment has a specific time limit, then not eligible for VSIP and/or VERA

- Title 42(f) - if appointment does not have a specific time limit (indefinite), the eligible for VSIP and/or VERA, provided other requirements are met for these incentives such as, being employed by the Executive Branch of the Federal Government for a continuous period of at least 3 years.

- How much is the VSIP? The incentive amount will vary by employee. The payment is the amount of severance pay you would get or $25,000--whichever is less. You can find a severance pay calculation sheet on OPM's website at Severance Pay Estimation Worksheet.

- When will I receive my buyout/incentive payment? It will be a lump-sum payment with your final paycheck.

- Is the VSIP taxable or subject to deductions? Yes. The payment is taxable and subject to other required deductions and/or debts.

- Federal, State, & Local Taxes

- Medicare & Social Security, as applicable

- Court Ordered Child Support/Alimony

- Debt Owed to the Agency

- Court Ordered Commercial Garnishments & Fees

- Can Veteran's Preference be applied for VSIP eligibility? No.

- Can the buyout payment be rolled into an IRA or another form of tax shelter? No. The buyout is fully taxable.

- Can I leave before the official separation period? Yes, but you will NOT receive the buyout/incentive payment.

- If I take the buyout, can I take a job in another Federal agency? Review the "Repayment Requirement" section on OPM's VSIP page.

- If I receive an eligibility notice for VSIP, will I be on administrative leave AFTER 05/09/2025? No. You MUST separate by 05/09/2025. Administrative leave must be taken between 03/17/2025 and 05/09/2025. Your last day of administrative leave and your separation date will be the same day.

- I took the buyout (VSIP) and not VERA. When must I separate from the agency? You may elect to be placed in an administrative leave status, receiving full pay and benefits for eight (8) weeks after you are approved for the VSIP. Once you are in an administrative leave status, no further obligation to report to duty is required and you may seek outside employment. You must be off NIH rolls by May 9, 2025.

- I took the buyout (VSIP) and am eligible for optional retirement. When must I separate from the agency? You must retire no later than May 9, 2025.

- I took the buyout (VSIP) and the VERA. When must I separate from the agency? If you are eligible for VERA by April 19, 2024, you must retire by this date. If you first become eligible for VERA between April 20, 2025, and May 9, 2025, you must retire on the date you meet eligibility. If you become eligible after 05/09/2025, you are not eligible for VERA.

- Am I required to take administrative leave? No. Administrative leave is 100% your choice.

- When will I know if I am eligible for the VSIP? Eligibility is a determination that must take place across multiple offices. An official email will be provided to inform you of your eligibility as soon as a determination is made. At that time, you may confirm you elect to move forward with the VSIP offer. The type of separation must also be confirmed. The date of separation needs to be communicated so that if you elect to be placed on administrative leave, your Administrative Officer (AO) and supervisor know how to process your timecard.

- I completed the VSIP Interest Form. Can I change my mind? Yes. A VSIP is voluntary, and coercion is prohibited. If you choose not to take the VSIP you will remain in your current position.

Deferred Resignation Program (DRP)

- Where can I find information from the DRP Session that occurred March 5, 2025? You can find a summary of additional FAQs and information from this session here.

- How long can employees who are resigning only stay on administrative leave? As late as September 30, 2025.

- How long can employees who are eligible for regular retirement between now and September 30, 2025, stay on administrative leave? As late as September 30, 2025.

- How long can employees who are FIRST eligible for regular retirement between October 1, 2025, and December 31, 2025, stay on administrative leave? As late as December 31, 2025.

- How long can employees who are retiring under the DRP VERA stay on administrative leave? December 31, 2025.

- Where can I find the VERA application and FERS application? There is one FERS application used for both regular and VERA retirement. All forms that need completed are located at FERS | Office of Human Resources.

- Will employees who accepted the DRP be paid for Time Off Awards (TOAs) if they are unable to use it before they are placed on administrative leave? No. TOAs cannot be converted to cash.

- Will employees receive payment for unused credit hours? A full-time employee receives pay for a maximum of 24 unused credit hours at his or her current rate of basic pay when Federal employment ends.

- How are lump sum payments for unused annual leave taxed? They will be taxed as income.

- What happens to unused sick leave? Unused sick leave will be used in the calculation of an employee's annuity if the employee is eligible for retirement. If the employee is not eligible for retirement, sick leave is frozen and can be restored if the employee ever returns to federal service.

- Can I still donate leave while on administrative leave? Employees use ITAS to donate leave. Since system accesses will be terminated once on administrative leave and employees will be unable to donate.

FEDERAL EMPLOYEE'S HEALTH BENEFITS (FEHB)

- What will happen to my health benefits as I transition to retirement? Your current health benefits coverage will transfer into retirement, provided you meet the eligibility requirements of:

- retiring on an immediate annuity; and

- have been continuously enrolled (or covered as a family member) in any FEHB Program plan (not necessarily the same plan), which includes both FEHB and PSHB health plans, for the five years of service immediately preceding retirement, or if less than five years, for all service since your first opportunity to enroll.

For employees who do not qualify under the preceding requirements, OPM has the authority to grant pre-approved waivers to employees who have been:- Covered under the FEHB Program continuously since the beginning date of an OPM approved VERA; and

- Retire during an OPM-approved VERA period and take the VERA offering.

- Can I suspend FEHB? Yes, under limited circumstances. As an annuitant, you can suspend your FEHB enrollment to enroll in a Medicare Advantage plan; TRICARE, CHAMPVA, Medicaid or a similar state-sponsored program of medical assistance for the needy; or use Peace Corps health insurance coverage. Later, if you lose your other coverage, you may re-enroll in a FEHB plan effective the date coverage was lost. If you do not lose your other coverage but want to re-enroll in a FEHB plan, you may do so during Open Season.

- Will my health benefits costs increase if they transfer into retirement? No, you will pay the same premium as you paid while you were an employee. As an annuitant, you will pay for health coverage through monthly withholding from your annuity, instead of paying through biweekly withholding from your paycheck (12 payments annually instead of 26 payments annually). Each payment will be higher when paid on a monthly basis.

- Will coverage I have under TRICARE/CHAMPUS count toward the FEHB five (5) year or first opportunity requirement? Yes, as long as you are covered under a FEHB enrollment at the time of retirement. In addition, you must have enrolled in the FEHB/PSHB Program within 60 days after you lost coverage under TRICARE for it to be considered part of the continuous FEHB coverage.

- What happens if I cancel my health benefits enrollment when I retire? If you cancel your FEHB enrollment as an annuitant, you will NEVER be able to reenroll, unless you become reemployed in a position that conveys coverage.

- If I cancel my FEHB enrollment to be under my spouse's FEHB enrollment, will I be able to reenroll under my own coverage at a later date? Yes. As long as you are continuously covered under a FEHB enrollment, you remain eligible to make any of the same enrollment elections or changes that an active employee would be eligible to make.

- Will a period of health benefits termination due to leave without pay (LWOP) greater than 12 months count as a break in the continuous coverage necessary for continuing FEHB coverage into retirement? No. The termination of your health benefits due to 365 days in LWOP status is not considered a break in the continuous coverage necessary for continuing FEHB coverage into retirement. However, the period during which the termination is in effect does not count toward satisfying the required five (5) years of continuous coverage. In addition, to meet eligibility requirements, you must have reenrolled in health benefits within 60 days of returning to pay status.

- If I'm eligible to carry FEHB into retirement, what options do I have in retirement? You can change your enrollment from Self & Family to Self+1 or Self Only at anytime. You can change plans during Open Season.

- Where can I find more information on health insurance in retirement? If you are eligible for VERA, you will receive further information from the NIH. You can also access additional information on the FEHB Program at Health Insurance | Office of Human Resources. As an annuitant, you can refer to OPM’s website at https://www.opm.gov/healthcare-insurance/ for information.

- If I am not eligible to keep my FEHB for any reason, what are the options for continuing my health insurance coverage? You have two options, as follows:

- You can convert to a nongroup contract (individual policy) with the carrier of the plan you are enrolled in at the time of your separation.

- You can elect 18 months of coverage under the Temporary Continuation of Coverage (TCC) provisions of the FEHB Program.

- How do I elect Temporary Continuation of Coverage (TCC)? You must complete and submit SF 2809, Health Benefits Election Form, to the Benefits Office within 60 days of the following, whichever is later:

- The date of separation.

- The date you received notification from the Benefits Office about options available for continuing your health insurance coverage.

- What plan choices do I have under TCC? You may choose any FEHB plan, option, or type of coverage that you are eligible to select. If you elect TCC, you will be responsible for the full premium cost plus a two percent (2%) administrative surcharge.

- If I elect one of the options available for continuing my health insurance coverage, when is coverage effective? The effective date of coverage for both options is the day after the expiration of the 31-day temporary extension. When TCC expires after 18 months, you will be entitled to a free 31-day temporary extension of coverage for the purposes of converting to a nongroup contract (individual policy) with the plan.

- Where can I find more information on health insurance? You can access additional information on the FEHB Program at Health Insurance | Office of Human Resources. As an annuitant, you can refer to OPM’s website at https://www.opm.gov/healthcare-insurance/ for information.

FEDERAL EMPLOYEES' GROUP LIFE INSURANCE (FEGLI)

- How can I carry FEGLI into retirement? You must have been enrolled into FEGLI basic and optional insurances for 5 consecutive years prior to your retirement date or since your first opportunity to enroll if less than 5 years.

- If I take a VERA, I will not meet the five (5) year requirement to continue my FEGLI optional coverage. Can I convert this coverage to an individual policy? Yes. After you are separated, the Benefits Office prepares a SF 2819, Notice of Conversion Privilege, Federal Employees' Group Life Insurance Program. This notice advises that your group life insurance coverage will terminate and gives you information about your right to convert to an individual direct pay policy. However, if you have assigned your life insurance coverage to another party, only the assignee (or assignees) may convert the insurance coverage.

- How much will a nongroup life insurance contract cost? The premiums for a nongroup life insurance contract will be determined by the type and amount of the coverage and your age and class of risk on the day following termination of your group coverage. You will be responsible for the total premium cost of the nongroup life insurance contract.

- If I elect to convert to a nongroup life insurance contract, when will coverage begin? If you elect to convert to a nongroup life insurance contract, your coverage and premium payments will be effective retroactive to the day after the 31-day temporary extension ended. Any insurance policy purchased under the conversion privilege is a private business transaction between you and the insurance company.

- What happens to my basic life insurance after I retire and reach age 65? Basic life insurance is your salary at the time of retirement rounded to the nearest $1,000 plus an additional $2,000.

- If you choose no reduction, you will continue to pay a premium and the policy will remain at full face value.

- If you choose 50% reduction, you will continue to pay a premium, and at age 65 the policy will begin to reduce by 1% per month until it reaches 50% of face value.

- If you choose 75% reduction, you will not pay a premium once you reach age 65, and the policy will begin to reduce by 2% per month until it reaches 25% of face value.

- What happens to Option A, Option B and Option C after I retire? If you have maintained optional coverage for a 5-year consecutive period leading up to your retirement or are otherwise eligible to continue your optional coverage, you can choose to keep Option A, Option B, and/or Option C in retirement. The cost of the coverage will vary depend on your life insurance elections and if you chose to decrease your coverage level.

- Option A – Gives you an additional $10K.

- If you continue it in retirement, you will pay a premium and the policy value will remain the same, but the premium will increase every 5 years until you reach age 65. Once you reach age 65, you will no longer pay a premium, however, your policy will reduce 2% per month until it reaches 0% of face value.

- Option B - multiples of your salary & Option C - for spouse and children (up to age 22).

- If you choose no reduction multiples, you will pay a premium and the policy will remain at full face value, but the premium will continue to increase every 5 years.

- If you choose full reduction multiples, you will continue to pay a premium and the policy will remain at full face value, but the premium will continue to increase every 5 years. At age 65, you will not pay a premium, but the policy will reduce 2% per month until it reaches 0% of face value.

- Option A – Gives you an additional $10K.

- Where can I determine the cost of FEGLI in retirement? You may compute the cost of your premiums using OPM’s FEGLI Calculator at https://www.opm.gov/retirement-services/calculators/fegli-calculator.

THRIFT SAVINGS PLAN

- Can I withdraw from TSP without an early withdrawal penalty? If you separate from the Federal Government in the year you turn 55 or older, you can withdraw funds from your TSP account without the 10% early withdrawal penalty for not being 59½.

- What happens to my TSP loan after retirement? If you have an outstanding TSP loan when you retire, you have three options:

- Pay off the loan by the required deadline; or

- Keep the loan active by setting up monthly payments by check, money order, or recurring direct debits. The payment will be changed to a monthly schedule, if necessary; however, the maximum time limit for paying off the loan will still apply.

- Allow the loan to be foreclosed and accept any taxable portion of the outstanding balance and accrued interest as taxable income.

- When I die after retirement, who receives the remaining balance of my TSP? If you do not file a Designation of Beneficiary form or have not recorded your beneficiaries at www.tsp.gov before the date of your death, your remaining balance will be distributed according to the order of precedence required by law.

- If I roll over my TSP account to an IRA after retirement, can I roll the funds back to TSP? Yes. TSP will accept both transfers and rollovers of tax-deferred money from traditional Individual Retirement Arrangements (IRAs), SIMPLE IRAs, and eligible employer plans such as a 401(k) or 403(b) into the traditional balance of your account. TSP will accept only transfers (i.e., direct rollovers) of qualified and non-qualified Roth distributions from Roth 401(k)s, Roth 403(b)s, and Roth 457(b)s into the Roth balance of your account. If you don’t already have a Roth balance in your existing TSP account, the transfer will create one.

- How can I find out how much I can get monthly from TSP? You can visit the TSP Payment and Annuity Calculator: https://www.tsp.gov/calculators/.

- What is the Required Minimum Distribution (RMD) for TSP? The Internal Revenue Code requires that you receive a portion of your TSP account (your required minimum distribution or RMD) beginning when you reach a specific age and are separated from service. TSP will initiate the required distribution to you by April 1 of the year following your separation. Refer to the table on TSP's website to see applicable age and required beginning date.

- If I retire under a VERA, are there any special TSP advantages, penalties, or rules? There are no differences in TSP provisions for retirement under VERA versus separation or optional retirement. You will have the same withdrawal choices and tax consequences as any other separated or retired employee with the same separation or retirement date and age.

- If I retire under a VERA, can I continue to contribute to TSP? No. Following retirement, you are not eligible to make additional contributions to or borrow money from your TSP account. You may continue to reallocate money among the TSP funds.

- If I retire under a VERA, can I withdraw funds from my TSP? Yes. If you retire, you will receive extensive information regarding your TSP withdrawal options and whether you may leave your money in TSP.

- How long will it take me to get my money from TSP? Withdrawal of funds may take at least two (2) months following separation and after the receipt of properly completed forms by TSP.

- If I withdraw money from my TSP account, will I have to pay taxes? If you retire before the year that you reach age 55, then any amount that you withdraw from your TSP account before you reach age 59½ is subject to an early withdrawal penalty tax of ten percent (10%). However, this penalty tax does not apply to amounts received under certain withdrawal options, such as an annuity or rollover to an IRA.

- Does my spouse have any rights concerning how I withdraw my TSP funds? Your spouse does have certain rights, as explained in TSP materials you will receive.

- Where can I find more information about TSP? If you are eligible for VERA retirement, you will receive further information from the HRSSC, which is your source for such information while you are an employee. After you separate, you must contact the TSP Service Office for assistance with your TSP account or if you have TSP questions. It is extremely important to inform the TSP Service Office of any changes in your address. A change of address form is included in the withdrawal package sent to you by the HRSSC. Contact the TSP Service Office at 1-877-968-3778, TDD (for deaf and hard of hearing participants) use 1-877-847- 4385; or access the TSP website at www.tsp.gov.

MEDICARE

- If I continue to work past age 65, is my FEHB coverage still primary? Yes. Your FEHB coverage will be your primary coverage until you retire. After you retire and enroll in Medicare Part B, then Medicare will be your primary coverage for eligible expenses and FEHB will be your secondary coverage.

- How do I obtain more information about Medicare? Call 1-800-MEDICARE (1-800-633-4227), TTY is available at 1-877-486-2048, or refer to the website: www.medicare.gov.

FEDERAL EMPLOYEE DENTAL & VISION INSURANCE PROGRAM (FEDVIP)

- Can I continue my FEDVIP dental and/or vision coverage into retirement? Yes. Your FEDVIP coverage automatically continues when you retire if you are enrolled as an employee. There is no 5-year requirement for continuing FEDVIP into retirement. To be eligible for FEDVIP as a retiree, you must have retired with an immediate annuity (a FERS MRA+10 annuity or postponed annuity counts as an immediate annuity). You can enroll in a FEDVIP dental plan and/or a FEDVIP vision plan for the first time as a retiree, even if you were never enrolled as an employee, as long as you have an immediate annuity. Those in receipt of a deferred annuity are not eligible to enroll in FEDVIP.

- Can I cancel my FEDVIP enrollment when I retire from the Federal government? You can only cancel your FEDVIP dental or vision enrollment during the annual Open Season or when you have a qualifying life event.

- Will my premiums change when I retire? No, your premiums or benefits will not change after retirement. Your premiums, however, will be post-tax and will be withheld from your monthly annuity.

- Do I need to contact BENEFEDS to let them know that I have retired and FEDVIP premiums need to come out of my annuity payments instead of my paycheck? You are not required to contact BENEFEDS. However, you can speed up the process of having premiums withheld from your annuity (so you have to catch up on fewer premiums) by contacting BENEFEDS.

In most cases, changing from payroll deduction to annuity deduction is automatic, but may take one to three months to occur because premiums cannot be deducted from your annuity while you are receiving "special" or "interim" pay. Once your annuity is finalized, premium deductions will begin, assuming your annuity is sufficient to cover the premiums.

If you miss one or more premium payments before your annuity is final, BENEFEDS may send you a direct bill which you must pay. If you do not pay the bills, your coverage may be cancelled.

- If I’m not enrolled now, and I retire, can I enroll during retirement? Yes, you can enroll during an Open Season as an annuitant.

- What happens to my dental and/or vision insurance (FEDVIP) if I am involuntarily separated by a RIF and I’m not eligible for retirement with an immediate annuity? You cannot enroll or continue FEDVIP enrollment after you leave the NIH. There is no 31-day temporary extension of coverage or opportunity to convert to private coverage. Your coverage ends on the last day of the pay period in which you separate. If you are only eligible for deferred retirement (this means you cannot receive a retirement annuity immediately, but you can receive an annuity at a future date) you cannot enroll in or continue FEDVIP.

- How do I contact BENEFEDS, and where can I find additional information about FEDVIP? You can find additional information at www.benefeds.gov or by calling 1-877-888-FEDS (3337), TTY 711.

FLEXIBLE SPENDING ACCOUNTS (FSA)

- Am I eligible to participate in FSA programs in retirement? No. By law, annuitants cannot participate in any FSA programs. FSAs are a way of setting aside pretax salary for reimbursement of eligible expenses. Annuitants receive annuities, which are not salary.

- What happens to your FSA funds when you retire?

- Your Health Care FSA or Limited Expense Health Care FSA will terminate as of the date of your retirement. There are no extensions. Any eligible health care expenses incurred prior to the date of retirement will still be reimbursed, but those incurred after the separation date are not reimbursable, even if you accelerated your allotments.

- You have until April 30 of the following year to submit claims towards your current year and carryover balance. Any balances remaining for which claims were not submitted by April 30 will be forfeited.

- Your Dependent Care FSA (DCFSA) remaining balance can continue to be used to pay for eligible dependent care expenses until your account balance is depleted or the end of the calendar year, whichever comes first.

- Your Health Care FSA or Limited Expense Health Care FSA will terminate as of the date of your retirement. There are no extensions. Any eligible health care expenses incurred prior to the date of retirement will still be reimbursed, but those incurred after the separation date are not reimbursable, even if you accelerated your allotments.

- Can annuitants participate in the FSA program? No. Under the IRS Code, annuitants (other than reemployed annuitants whose employment status is full-time) cannot participate in FSA.

SICK LEAVE

- Will I get a lump sum payment of my unused sick leave at retirement? No, accumulated hours of sick leave are not paid in a lump sum at the time of retirement. Sick leave hours are converted into creditable service and may increase your overall annuity payment.

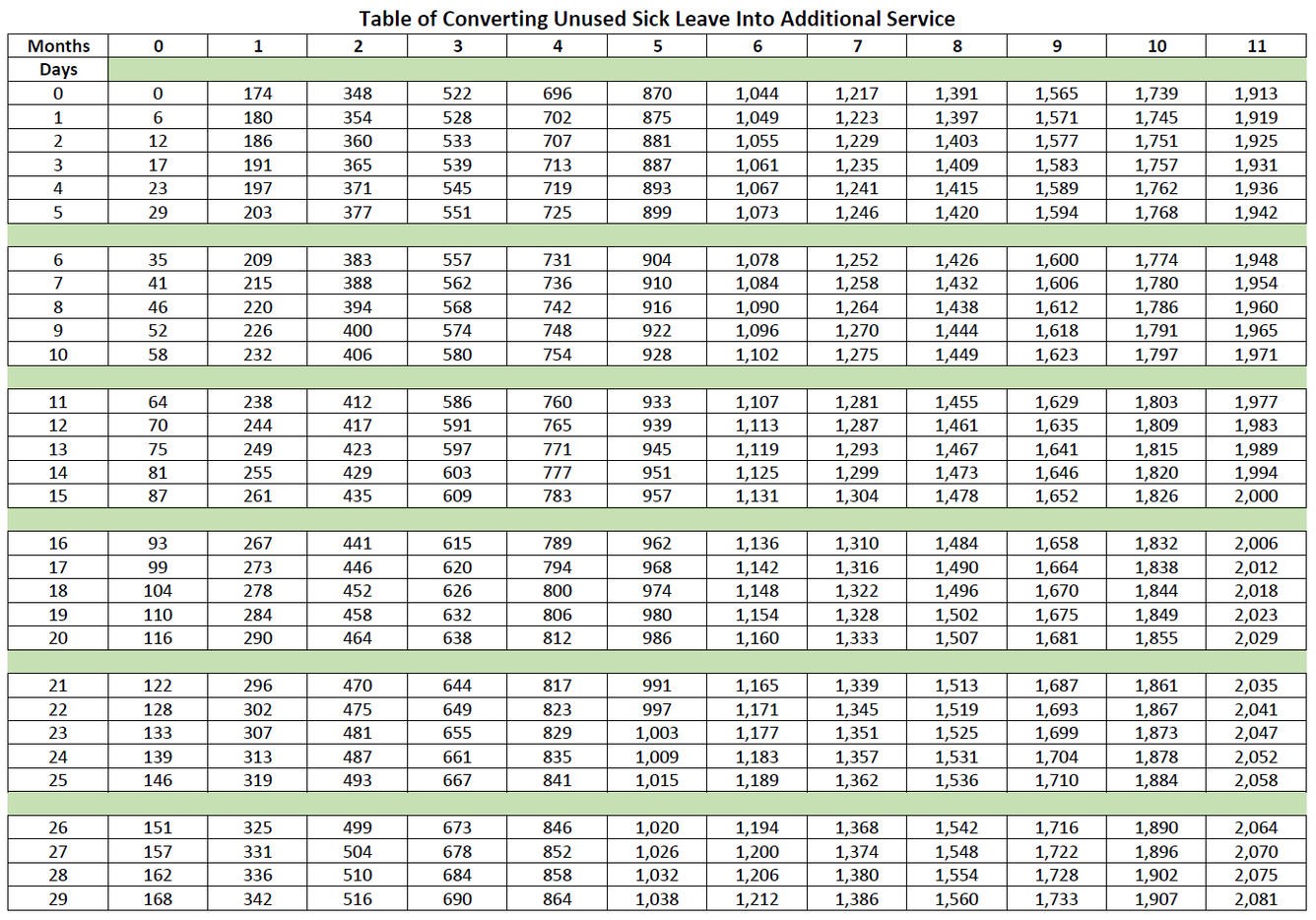

- How is sick leave converted into retirement? Your sick leave is converted to years, months, and days that are added to your total actual service at retirement eligibility using the 2087 Sick Leave Conversion Chart at: https://hr.nih.gov/sites/default/files/public/images/2025-03/Sick-leave-conversion-chart.jpg. Your service credit and sick leave will be combined to determine your total service credit. Your annuity will be computed with only your total service credit, using only years and whole months of service. Note: One year of creditable service is equivalent to 2087 sick leave hours.

- Can I request to use sick leave prior to the effective date of retirement? Certainly. NIH sick leave policy continues to apply. Sick leave used prior to the effective date of retirement may affect your total service credit by decreasing your total actual service. This may affect your annuity. The annuity estimate you received was only an estimate. OPM is the agency that adjudicates your final retirement and annuity payment.

- Does sick leave count towards FERS Annuity Supplement? No, sick leave hours are not included when calculating the Special Supplement Annuity.

- If I separate from the NIH under a VERA, what will happen if I am indebted to the NIH for advanced sick leave? If you are indebted to the NIH for unearned annual or advanced sick leave, you must refund the amount paid for the unearned leave. If you do not refund the amount of the indebtedness, deductions will be made from any funds paid to you upon your separation and/or the NIH may seek to recover the debt.

{kind=link}

ANNUAL LEAVE

- What is a final leave check? A final leave check is a lump-sum payment for earned annual leave upon separation.

- Is there a maximum amount of earned annual leave I can receive in a final leave check? No, not when separating under a VERA. Employees may receive a lump-sum payment for:

- Accumulated annual leave carried over from the previous year;

- Accrued annual leave for the year in which they separate, including amounts over the applicable carryover maximum;

- Any unused donated leave; and

- For full-time and part-time regular employees, holidays that fall within the final leave period.

- What rate of pay is used for the final leave payment? Final leave is paid at the salary rate in effect at the time of the employee's separation. Final leave payments can be direct deposited.

- When will I receive the final leave check after retirement? The final leave check is issued one or two pay periods after the effective date of retirement or two pay periods after the separation action is processed.

- If I separate from the NIH under a VERA and have earned and unused annual leave, will I be paid holiday leave for any holidays that occur after my separation date but before my annual leave would be exhausted? Yes. Annual leave is spread over the appropriate number of days following your separation date and extended one day for each federal holiday that occurs during that time period. For example, if you have 160 hours of earned and unused annual leave and two holidays would occur in the four weeks (40 hours per week) after the date of your separation, you would receive final leave pay for 176 hours (160 hours of earned and unused annual leave plus 16 hours of holiday leave).

- If I separate from the NIH under a VERA, what will happen if I am indebted to the NIH for unearned annual leave? If you are indebted to the NIH for unearned annual or advanced sick leave, you must refund the amount paid for the unearned leave. If you do not refund the amount of the indebtedness, deductions will be made from any funds paid to you upon your separation and/or the NIH may seek to recover the debt.

- What deductions are withheld from the annual lump sum leave payment? Federal, State, Medicare, and Social Security taxes, if applicable, are withheld from this payout.

Post Retirement - Other

- What happens after retirement? Refer to OPM's Retirement Quick Guide for what to expect from OPM upon your retirement.

- How do I set-up my Service Online account? Refer to OPM's tutorial on how to establish your account access.

- What can I do in my Services Online account? Services Online options are limited during your Interim Pay status. After that, you can do the following:

- Start, change, or stop Federal or state tax withholdings.

- Start, change, or stop allotments to financial institutions.

- Change your mailing address or Direct Deposit information.

- View a statement describing your annuity payment.

- View/print your annual CSA 1099-R (“retiree W-2”).

- Will Federal income taxes be withheld from my annuity? Yes- Federal taxes will be based on the same marital status and number of allowances being used to tax your salary.

- Will State income taxes be withheld from my annuity? No, State taxes are not automatically withheld.

- State taxes cannot be withheld until your retirement is finalized.

- Because of the OPM’s processing times, you may need to make estimated payments.

- Once your retirement is finalized, you may request state taxes be withheld from your annuity by contacting OPM to request the dollar amount you want withheld.

- Contact your state tax office to help you determine the appropriate withholding.

- Who do I contact once my retirement is final? OPM's Annuitant Services at www.opm.gov/support/retirement/contact.